Why is the 3D market split into two?

The global 3D printing market reached 16 billion dollars in 2025, growing by 10% annually. But this recovery hides deeply diverging dynamics: entry-level systems under $2,500 are recording growth above 30%, while high-end industrial platforms continue to suffer from slow and cautious investments.

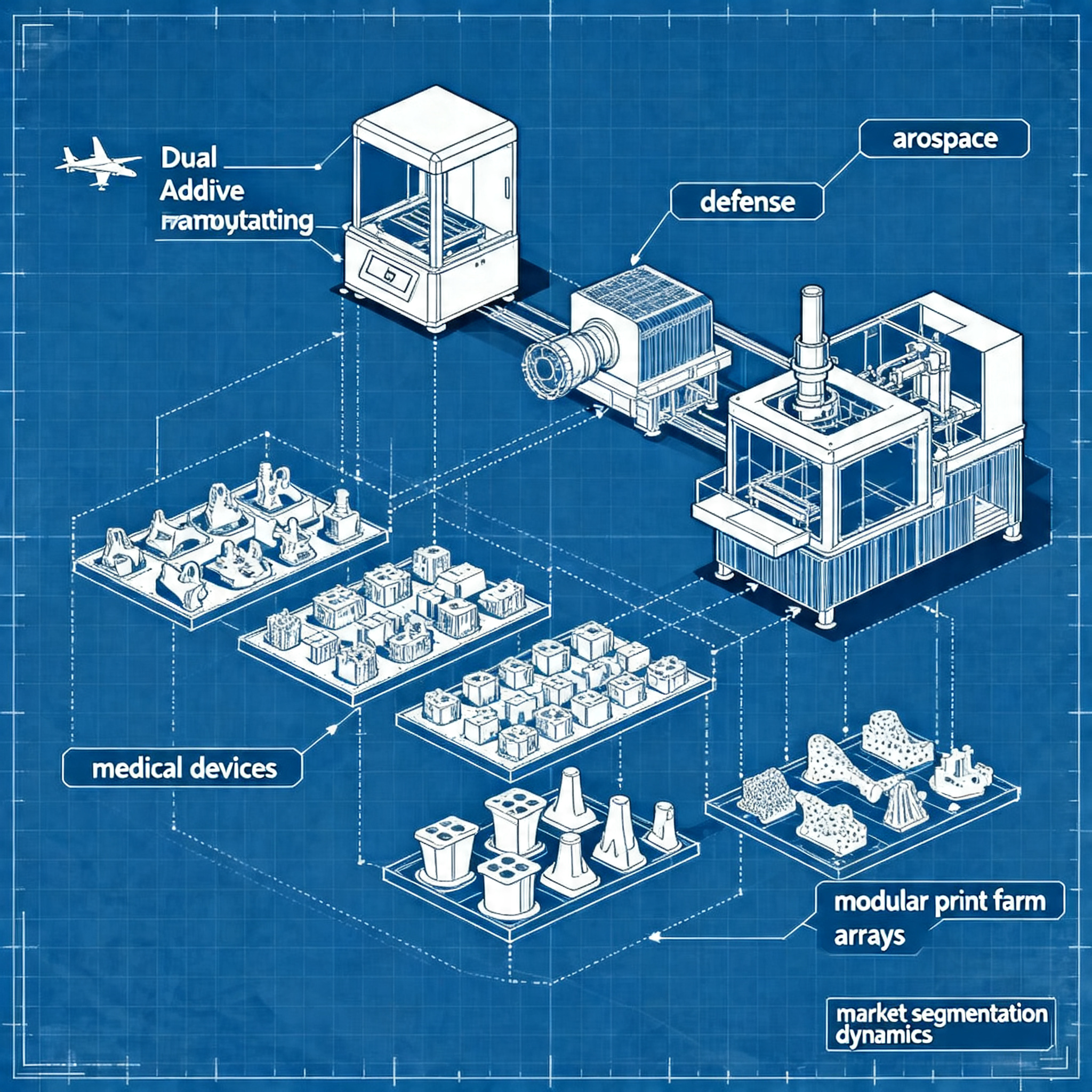

The split doesn't concern only the price. Three specific industrial sectors — aerospace, defense and healthcare — are driving the demand for professional systems, while the rest of the industrial market remains in a consolidation phase. Meanwhile, the consumer and maker segment is accelerating with completely different logics.

Split growth: who accelerates and who brakes

Market expansion shows two faces: on one side entry-level systems and on the other high-end industrial ones, with clearly different trends.

In the third quarter 2025 global hardware revenues grew by 5% year over year, but this average hides a clear split. Printers under $2,500 recorded growth above 30%, while systems between $20,000 and $100,000 saw shipments drop by 13%.

- Entry-level systems (under $2,500): +30% year over year

- Mid-range ($20,000-$100,000): -13% in units shipped

- Industrial Metal PBF: +25% driven by China, aerospace and defense

- Industrial systems above $100,000: +3% in units, but demand remains cautious

The CONTEXT data shows that demand for entry-level systems no longer comes only from hobbyists. Industrial companies are building “print farms” with dozens of low-cost machines instead of investing in single industrial systems costing hundreds of thousands of dollars. This approach reduces capital risk and increases production redundancy.

On the opposite side, industrial platforms above $100,000 are growing only 3% in units. Macroeconomic uncertainty, trade tariffs, and the weakness of the European manufacturing sector are weighing on investment decisions. The market has shifted from a phase of “expansion at any cost” to a focus on sectors where AM generates clear economic value.

Leading sectors: aerospace, defense, and healthcare

Three industrial sectors are driving demand, with applications ranging from rapid prototyping to direct additive production.

AM Research identifies three verticals with growth rates above 20% annually over the last four years: medical/dental, aerospace, and defense. These sectors no longer use 3D printing as an experimental technology, but as a core production method.

In the space sector, rocket engine production represents one of the most significant value drivers for the next decade. Military OEM manufacturers and defense sector startups are using AM to solve supply chain issues and produce drones and next-generation components.

| Sector | Annual growth | Main applications |

|---|---|---|

| Aerospace | >20% | Rocket engines, lightweight structural components |

| Defense/Maritime | >20% | Drones, on-demand spare parts, resilient supply chain |

| Medical/Dental | >20% | Custom implants, surgical guides, dental prosthetics |

3D Systems has confirmed that medical tech, dental, and aerospace/defense are the three markets it is focusing on for product development. These sectors offer sustained growth opportunities for the next decade, with regulatory barriers protecting margins and increasingly integrated workflows.

China represents a particular case: shipments of metal PBF systems grew by 35% year-over-year, with most machines remaining in the domestic market. Chinese customers operate primarily in aerospace and the private space sector.

The gap between makers and industry is widening

The needs of the hobbyist market and those of the industrial sector are becoming increasingly non-overlapping, requiring distinct approaches.

The desktop segment under 10,000 euros is no longer reserved for hobbyists. AMPOWER finds that this sector is gaining industrial relevance, with companies investing in low-cost printer farms instead of relying exclusively on expensive single industrial systems.

This evolution challenges traditional market classifications. Entry-level printers now offer sufficient precision and reliability for low-volume productive applications, while reduced operating costs enable economies of scale that are impossible with industrial machines.

Industrial companies no longer see entry-level systems as alternatives to professional ones, but as complementary. A farm of 20 printers at 3,000 dollars costs 60,000 dollars compared to 150,000-300,000 for a single industrial system, offering greater redundancy and flexibility.

On the opposite front, high-end industrial systems focus on applications where quality, certification, and repeatability are critical. Metal PBF for certified aerospace components, systems for custom medical plants, and large-format platforms for serial production require investments that the maker segment cannot justify.

The result is an increasingly segmented market, where product, pricing, and go-to-market strategies must be radically different. Vendors that try to cover both segments with the same approach risk losing relevance in both.

Penetration strategies for separate segments

Companies must redefine their market strategies to address the specific needs of each segment without compromises.

The divestitures of non-core assets by 3D Systems (Geomagic to Hexagon for 123 million), TRUMPF (AM business to DUBAG/LEO III), and Materialise (RapidFit via MBO) signal a clear trend: vertical specificity beats horizontal coverage.

Businesses that thrive after restructuring are narrowly focused. Stratasys targets FDM consumables, aerospace, and dental. Materialise Medical focuses on custom implants and software. ATLIX (formerly TRUMPF AM) aims at medical and aerospace with full-service application consulting.

Strategic approach by segment

- Entry-level/Maker: Focus on volumes, ease of use, content ecosystem, and community. Margin comes from scale and recurring materials.

- Generalist industrial: Focus on 2-3 specific verticals with integrated workflows. Avoid spreading across too many sectors.

- High-end certified: Invest in material qualification, process certifications, and application support. Value lies in reducing customer risk.

AM Research predicts that services will become the largest segment over time, surpassing hardware and materials. This reflects a transition from “selling machines” to “selling certified parts” or “guaranteed production capacity”. Companies that cannot compete on this dimension risk being marginalized.

The 13.51% annual growth forecast until 2029 from AMPOWER confirms that the market continues to expand. But this growth will not be distributed evenly: it will concentrate in segments where AM solves real economic problems, not where it is adopted for experimentation or technological hype.

The future of 3D printing will depend on the ability to adapt to the divergent dynamics of market segments. Companies that attempt to serve both makers and the aerospace industry with the same strategy risk

article written with the help of artificial intelligence systems

Q&A

What is the annual growth rate of the global 3D printing market in 2025?

The global 3D printing market grew by 10% annually in 2025, reaching $16 billion.

How do the performances of entry-level and industrial systems differ in the third quarter of 2025?

Entry-level systems under $2,500 saw growth exceeding 30%, while industrial systems priced between $20,000 and $100,000 experienced a 13% decline in shipments.

Which industrial sectors are driving demand for advanced 3D printing systems?

Aerospace, defense, and healthcare are the three sectors driving demand, with applications ranging from rapid prototyping to direct production of components.

Why are industrial companies preferring fleets of entry-level printers over expensive single systems?

Companies are building 'print farms' with low-cost printers to reduce financial risk, increase production redundancy, and achieve economies of scale impossible with individual industrial machines.

How is the role of entry-level printers changing in the industrial context?

Entry-level printers are no longer seen as alternatives to professional systems but rather complementary solutions, thanks to their increasing accuracy and reduced operating costs.